On 3 September 2025, the 56th GST Council meeting occurred, and a press release was issued containing the recommendations of the council meeting. Following is a brief of the said recommendations and opening thoughts on the same. The suggested changes are categorised as ‘Rate Changes’ and ‘Measures for Trade Facilitation’, as discussed hereunder.

Rate Change – Services:

- Insurance – Significant impact for the insurance industry as health insurance and life insurance (incl. reinsurance) is proposed to be exempted – this can cause harm rather than benefit the sector and its players, as the ITC chain would be broken. Immediate analysis needs to be done to find the right balance.

- Job work activity – Significant relief as the rate of tax has been substantially reduced from 12% to 5%.

- Transportation Sector – Increase in rate of services; however, a decrease in the rate of tax on goods vehicles and some ancillaries and accessories might balance the position swiftly.

- Construction Sector – No major change – except rate change of works contract involving predominantly earth work provided to the Government to be changed from 5% to 12%. However, a reduction in the rate of goods such as Sand lime bricks or Stone inlay work from 12% to 5% would have some impact.

- Hotel & Restaurant – Hotel accommodation of less than Rs. 7500 – rate reduced from 12% to 5%. Regarding restaurants, explanations should be added to clarify that a stand-alone restaurant cannot declare itself as a ‘specified premises’ and cannot avail the option of paying GST @18% with ITC. [No change]

- Mining and Exploration – a general increase in the rate of tax as composite supply of works contract and associated services, in respect of offshore works contract relating to oil and gas exploration and production in offshore area has been raised from 12% to 18%. Other professional, technical, and business services relating to exploration, mining, or drilling of petroleum crude or natural gas or both have also increased from 12% to 18%.

Rate Change – Goods:

- Food items: Significant change in the rate of various food items of daily use, starting from pizza bread to Paratha/Parotta to pistachios to Brazil nuts, cheese, ice cream, dried fruit, packaged coconut water, etc.

- Agriculture sector: Reduction in rate regarding various agricultural implements and equipment such as tractors, trailers, irrigation equipment, parts and accessories of tractors, some fertilisers, inter alia – this would lead to some relief to the farmers as well as users.

- Coal – in order to dissuade users, the GST has been increased from 5% to 18%.

- Renewable energy – Reduction in rate in respect of renewable energy equipment, such as solar cookers and solar power-based equipment and fuel cell vehicles, including hydrogen vehicles.

- Textiles – significant rate reduction in respect of various items such as yarns, non-wovens, carpets, quoted textile fabrics, textiles for technical usage, etc. Base rate for application of higher GST rate has also been increased in respect of various goods.

- Health – reduction in rate of tax in respect of rubber gloves, spectacles, blood sugar measuring devices and strips, various chapter 30 goods (pharmaceuticals), and goods falling under chapter 90 (instruments and equipment).

- Common man items – an interesting classification – GST reduced on various goods such as tooth powder, feeding bottles, umbrellas, sewing needles and machines, aluminium utensils, combs, bicycles, talcum powder, hair oil, shaving cream, shaving lotion, etc.

- Consumer electronics – reduction in the rate of tax on air conditioners, dish washing machines, televisions, monitors, and projectors, etc., from 28% to 18%.

- Paper industry – significant reduction in rate of tax on various items, such as wood pulp of different varieties, items made out of corrugated paper or non-corrugated paper or paper board, moulded items, biodegradable bags, chemicals used in the paper industry, etc.

- Transportation – reduction in rate of tax from 28% to 18% in respect of sub 4 metre passenger vehicles of engine capacity less than 1200cc (petrol/LPG/CNG) and 1500cc (diesel), ambulance, three wheelers, sub 4 metre hybrid vehicles, transport vehicles, parts, accessories, chassis and bodies of the above, motorcycles of up to 350cc, etc. The rate of tax on engines and engine parts of chapters 84 and 85 has also been reduced from 28% to 18%. Increase in rate of tax from 28% to 40% in respect of vehicles, having higher engine capacities or exceeding the 4 m length barrier, airport for personal use, motorcycles of more than 350cc, yachts and other vessels for pleasure or sports. – These changes are going to have a significant impact and are going to shape the future of the industry.

- Leather and wood – reduction in the rate of tax from 12% to 5% in respect of various raw materials and intermediate materials.

- Handicrafts – reduction in rate from 12% to 5% in respect of various items, such as idols made of wood, stone, metals; statues, paintings, and hand-painted articles, antiques, stoneware, bamboo goods, handmade paper, etc.

- Unmanned aircraft – The rate of tax on unmanned aircraft has been brought down from 28%/18% to 5% – this will add to the country’s capability in the field of multifarious usage of drones and unmanned aircraft.

- Defence equipment – reduction in the rate of tax in respect of various defence equipment.

Measures for Trade Facilitation

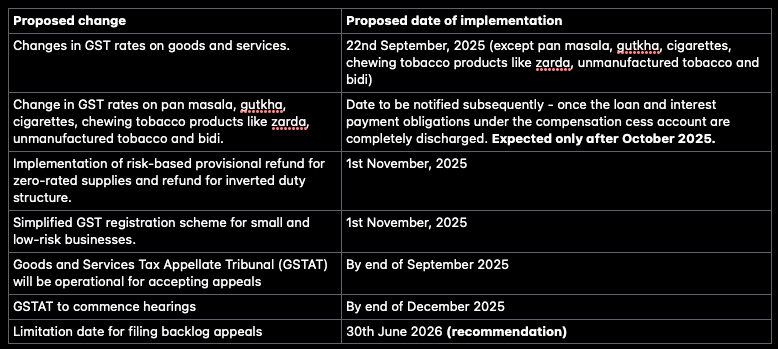

- Provisional refund for zero-rated supply of goods or services to SEZ units/ SEZ developers for authorised operations – Similar to exports, a provisional refund in respect of the supply of goods or services to SEZ units and SEZ developers is proposed to be from 1st November 2025.

- Provisional sanction of refund arising out of inverted duty structure – it is proposed that 90% of the refund claimed would be sanctioned on a provisional basis in respect of the refund arising out of the inverted duty structure. Proposed to be operationalised from 1st November 2025. – This would give relief to many industries and reduce litigation.

- Proposed amendment in section 13 of the IGST Act – Section 13(8)(b) of the IGST act, prescribe that place of supply in respect of intermediary services would be the location of the supplier of service – therefore, intermediary services provided from India to foreign clients are not treated as exports – however, on implementation of above amendment, intermediary services provided from India, to foreign clients would be treated as exports and Indian service providers would be able to avail the benefit of undertaking such exports. This is a major relief to service providers across the board.

- Relaxation of norms relating to post-sale discounts: It is proposed that there would not be any requirement to establish the existence of an agreement for the grant of a discount, and issuance of a credit note under Section 34 of the CGST Act would justify the discount. Therefore, the requirement of production of a CA certificate and additional supporting documents to the above effect, as is presently done, would also be dispensed with. Further, various clarifications are also expected to be issued in the form of circulars.

Changes for small taxpayers

- GST refund in respect of low-value export consignments – The CGST Act provided for a refund only in cases where the refund amount was more than ₹1000. This threshold limit is proposed to be removed in order to support small exporters, making exports through courier, postal, or other modes.

- Simplify GST registration scheme for small and low risk businesses – optional simplify GST registration scheme to be introduced where registration would be granted on automated basis within three working days from the date of submission of application in respect of lower risk applicants and where applicants on the basis of their own assessment, determine that their output tax liability to registered persons would not exceed ₹2,50,000 per month (including GST). Opting for an opting out of the scheme would be voluntary.

- Simplified registration scheme for small suppliers, supplying through electronic commerce operators – a special framework is proposed to be introduced.

The proposed implementation dates are as follows:

The complete press release dated 03.09.2025 can be accessed here.